Allied REIT is Stupid Cheap

Allied REIT is Stupid Cheap

Thinking back to 2021 the most talked about phrase in real estate was the Death of Retail (specifically, the mall). So obvious was this fact that we began imagining our entire world in a completely different way - sans mall. The only problem was it wasn’t true.

Today we are witnessing a repeat of essentially the same dumb extrapolation of a short-term trend said by the same dumb people, except with offices. Remote work is going to change the world. People are more productive and happier at home. Both true.

Working from home is indeed more productive. No commute makes anyone happier. Organizations are objectively more efficient running-in-place through remote work but they do not build culture, push forward, or educate the next generation behind a computer screen in their pyjamas. We are social animals and offices enable that innately human need. That is the optimistic / positive take. The cynical take is that bosses want to monitor their workforce and proximity to your superior increases your chance of promotion and reduces your chance of getting fired. Also true - both perspectives are valid and are at play. Recent trends in office utilization can also, in a sense, simply be viewed as the relative bargaining power of labour versus capital. When labour is tight they get to squeeze better conditions (like working from home). When labour becomes more available employers get to retract privileges (and then some).

Most importantly the elephant in the room is that office fundamentals for Class A properties (occupancy and leasing) have bottomed and turned the corner. Not everywhere, but in enough places and especially in the leading edge cities (like NYC) such that a trend is clearly discernible.

Per CBRE’s Q4:

We expect leasing to grow modestly in 2024. We are cautiously optimistic that the worst is over for office leasing, particularly for Class A properties, where we generate approximately 2/3 of leasing revenue. Leading indicators from our data partner, VTS, indicate U.S. office demand has been gradually turning up over the last 6 months.

The growing consensus about an economic soft landing, coupled with the apparent stabilization of office utilization rates may make more employers confident enough to commit to office leases.

Well. It is the case that we think it has bottomed out. It obviously is below where -- meaningfully below where it was, occupancy is -- square footage per person is below where it was, per employee is below where it was in 2019. There is all kinds of anecdotal evidence around that issue. Some stubbornness about people coming back to the office. That's super clear. The other thing is there's just a clear amount of pressure from companies to get their people back into the office for all kinds of reasons.

What we do know, and I would say anecdotal evidence in this area is not just evidence, it's an avalanche of evidence. Every company that you talk to, you can't talk to a corporate that would tell you that office building occupancy, either in buildings they own or building they lease, is not important to their business. It's important to all of them. It's important to us in our business. And so what you're seeing is that people are redoing their space, trying to make it a better environment for their employees, make their employees more efficient, more engaged.

Class A buildings that create that opportunity are seeing in a number of markets record rents. Buildings that aren't good are struggling, and they're going to continue to struggle. So we look at that circumstance, and we say there's pressure on both sides, but we think it's kind of stabilized. We think it will be a very big asset class going forward, bigger than the headlines might suggest because people tend to like negative news.

Vornado and SL Green are both reporting improving leasing and tours; NYC got hit first and these two quintessential NYC Class A office REITs are now on the upswing (just look at their share prices). As owners of some of the best buildings in NYC these REITs are the first-to-move and the prime beneficiaries of an office recovery as organic demand is naturally going to go first to the highest quality available (amenities, transportation) at a still-great price. The recovery in Class A space more broadly is also being supported by a draining of demand from Class B and Class C space as those tenants find that they have to upgrade their space in order to attract their workforce to the office and can, for now, do so at an attractive price relative to their historical rents.

The underlying fundamentals driving this recovery are no different between most cities in North America and Europe. There will be idiosyncratic factors that drive some outliers but the overwhelming majority of organizations are increasingly achieving increased attendance in-office and driving demand for the highest quality workspace.

Why Allied?

What makes Allied Properties (TSE:AP) stand out as Canada’s pre-eminent office REIT is some of the most attractive offices in North America and a massive hidden equity kicker. Here’s how Allied describes their properties:

DISTINCTIVE URBAN WORKSPACE: Allied was known initially for its leading role in the emergence of Class I workspace in Toronto, a format created through the adaptive re-use of light industrial structures in the Downtown East and Downtown West submarkets. This format typically features high ceilings, abundant natural light, exposed structural frames, interior brick and hardwood floors. When restored and retrofitted to high standards, Class I workspace can satisfy the needs of the most demanding office and retail users. When operated in a coordinated manner, this workspace becomes a vital part of the urban fabric and contributes meaningfully to a sense of community.

Here are some examples:

While these extremely attractive premium spaces may have formed the original core of the portfolio Allied also owns and has been developing almost all of Canada’s AAA new workspaces, for example The Well - a city-within-a-city mixed use building with office, retail, and residential that is a JV with Riocan REIT.

An Allied JV (with Westbank) is also finishing 400 West Georgia, a stunning building that will almost certainly be Vancouver’s pre-eminent business address for decades to come.

Allied has some of the most desirable offices in Canada and is primed to be the first port of call when demand inevitably picks up. Which leads us to the opportunity created by an uncertain outlook for 2024 from the Q4 call,

OUTLOOK

Consistent with the practice of most Canadian public real estate entities, Allied does not provide formal guidance. It has in recent years provided an annual outlook with respect to three non-GAAP metrics, FFO per Unit, AFFO per Unit and Same Asset NOI. Over the course of 2021 and 2022, these metrics were up. In 2023, these metrics were flat or down slightly. While Allied will strive for flat metrics in 2024, Management recognizes that the metrics may contract by up to five percent in the year. Management expects the metrics in the first half to contract, as it assumes no economic occupancy gains in that period. Management does expect economic occupancy gains in the second half of the year, but cannot be certain as to the magnitude of those gains, given the current macroeconomic environment.

If one assumes, as we do, that office fundamentals have turned the corner on a recovery and that fundamentals in Canada generally track but lag those of the United States (longer COVID lockdowns in Canada led to a delayed return to work but these economies are essentially joined at the hip) then this uncertain outlook makes sense. We expect this turnaround to start this year, boosted over the medium and long term by a booming Canadian population that should drive proportional workspace demand growth above and beyond what is seen in the United States. Allied is seeing the early innings of a recovery similar to what happened in the US last year - increased interest but hesitancy to commit, and it is simply a matter of when, not if, fundamentals track what we have already seen in leading US office markets.

From the same Q4 call,

Allied: Tour activity continues to be strong. We observed a 20% increase in tours in the quarter compared to the prior year. In total, tour activity was 12% higher in 2023 compared to 2022, with a noticeable acceleration of tours in the second half of the year.

Question: I guess I won't call it guidance, but on your -- the outlook that you put out in your press release, I'm just trying to square your comments on leasing and leasing activity seemed fairly constructive or positive. And I'm just trying to square that with the fact that you don't expect any occupancy gains in the first half of the year on your outlook?

Allied: It's really just a function of the extended lease-up time frames. So there might -- there will be leasing accomplished. But in terms of, let's say, cash generating leasing, we're expecting that to start in the second half of the year.

Here’s Allied’s occupancy as of Q4:

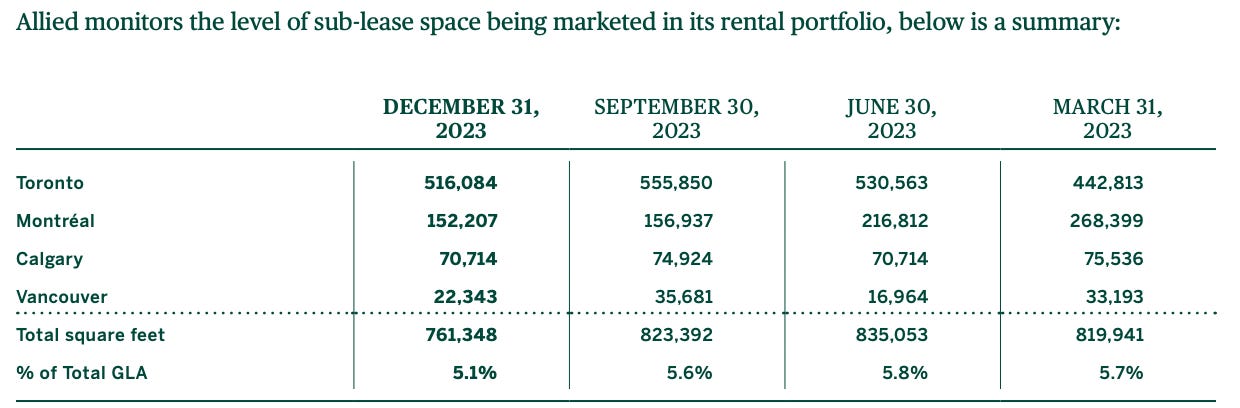

Despite the decrease in direct occupancy, sublease space is going in the right direction, which is a leading indicator for direct leasing:

The company has a very low amount of debt after selling off a data centre portfolio:

With a very manageable lease maturity:

And a very conservative financing schedule:

The current dividend results in a payout ratio of 82.7% of AFFO. Even if the worst case scenario of a 5% decline in AFFO in 2024 comes to pass we do not see the dividend being cut unless occupancy further deteriorates and/or rates increase into 2025. Allied maintains very healthy leverage ratios with a majority of its pipeline that has contributed to debt but contributed little to no income soon to be completed and mostly pre-leased. Right now a lot of that pipeline contributes to debt but not to income. Allied also has $500m in loans outstanding to residential developer Westbank, mostly in JVs, a substantial amount of which will be repaid as those projects complete either in cash or converted into very attractive equity ownership in those projects. Allied’s financial position is solid, and with a 10% dividend yield that is going to continue growing for many years you are being paid very generously to wait out the short term storm.

The Kicker and Value

Keep reading with a 7-day free trial

Subscribe to LF Research to keep reading this post and get 7 days of free access to the full post archives.